Asset retirement obligations

Background

The Public Sector Accounting Board (PSAB) PS 3280 – Asset Retirement Obligations standard was established to guide public sector entities on how to account for and report legal obligations associated with the retirement of tangible capital assets. This standard is exercised in conjunction with existing standards PS 3150 Tangible Capital Assets. This standard will replace PS 3270 Solid Waste Landfill Closure and Post Closure Liability when PS 3280 comes into effect.

Scope

Asset Retirement obligations (AROs) are legal obligations that result from a past transaction or event. This can occur from acquisition, construction, development, or normal use of a tangible capital asset. It is this, and not the existence of the contract, agreement, legislation, or other legally enforceable right that is the obligating event. Delaying the settlement does not relieve the entity of the obligation. The obligating event occurs when the asset is acquired. If an asset that was not previously required to be retired must now be retired due to new legislation, an ARO would be created when the legislation is enacted. This obligation would not be reported as a prior period adjustment since new legislation is a current period event.

Obligations that arise solely from a plan to sell or otherwise dispose of a tangible capital asset are outside the scope of this section.

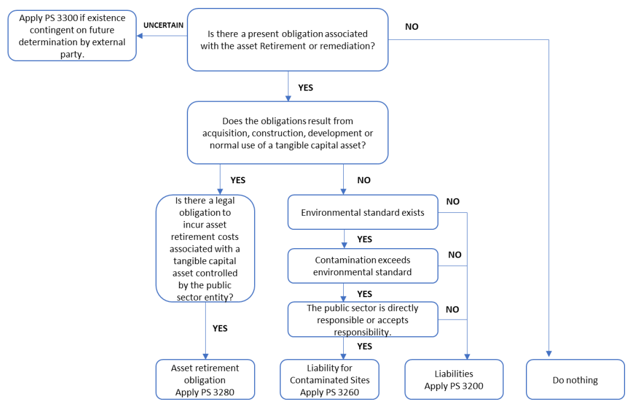

In certain circumstances, an entity may have doubts on whether there is an existence of an ARO. An assessment should be undertaken to determine whether obligations should be recognized or disclosed under PS 3260 Liability for Contaminated Sites, PS 3200 Liabilities, PS 3300 Contingent Liabilities, or PS 3390 Contractual Obligations.

See decision tree when assessing scope of liability:

Definitions

See reference PS3280.08-.10:

Asset Retirement Activities: These include all activities related to an asset retirement obligation. Examples include but are not limited to:

- decommissioning or dismantling a tangible capital asset that was acquired, constructed or developed;

- remediation of contamination of a tangible capital asset created by its normal use;

- post-retirement activities such as monitoring; and

- constructing other tangible capital assets to perform post-retirement activities.

Asset Retirement Cost: The estimated amount required to retire a tangible capital asset.

Asset Retirement Obligation: A legal obligation associated with the retirement of a tangible capital asset.

Present Value Technique: A method used to evaluate the present value of cashflow required to settle future obligations.

Legal obligation: A legal obligation establishes a clear duty or responsibility to another party that justifies recognition of a liability.

Recognition

An ARO should be recognized when the following criteria are met:

- there is a legal obligation to incur retirement costs in relation to a tangible capital asset;

- the past transaction or event giving rise to the liability has occurred;

- it is expected that future economic benefits will be given up; and

- a reasonable estimate of the amount can be made.

Asset retirement obligations should be assessed concurrently with the Province’s Asset Management policy. In addition to newly purchased assets and assets with a remaining useful life, an ARO will also apply to:

- Obligations associated with fully amortized tangible capital assets.

- Obligations associated with unrecognized tangible capital assets (including Crown lands.)

- Obligations associated with tangible capital assets no longer in productive use.

AROs exclude:

- Retirement obligations that are not legal obligations;

- Costs related to remediation of contaminated sites, which are covered in PS 3260;

- Costs related to activities necessary to prepare a tangible capital asset for an alternative use;

- Costs resulting from an unexpected event such as an unexpected contamination.

AROs must be evaluated and distinguished from other activities including reclamation and remediation. However, if these activities must be performed prior to an entity being able to retire an asset, these activities should be included into the total asset retirement cost.

AROs must be allocated on the same basis as the asset. The obligation and timing of settlement of a retirement obligation as well as the schedule of amortization should be consistent with the underlying component.

AROs must be amortized in a systematic and rational manner. An ARO’s useful life will be consistent with the current TCA policy in CPPM Chapter I.

For fully amortized tangible capital assets that are still in productive use, the ARO’s accumulated amortization is recognized to accumulated surplus upon implementation. New AROs that arise after implementation are expensed.

Example:

- For a building that has a remaining useful life of ten years, the ARO will be measured at either the date the asset was acquired or the date of the obligation, whichever occurs last. The amortization recognized is allocated based on the useful life of the underlying asset.

If the building was built in 1985, the estimated useful life is 40 years and it has an acquisition cost of $5,000, the building is expected to be demolished in 2025. The legislation was enacted in 1990. The ARO for this building is estimated to be $300.

The ARO would be adjusted to when the act came into effect, accumulated amortization would be adjusted from 1990, and the residual amortization expense would be recognized to 2025. (For a period of 35 years.)

As at April 1, 2022, the building’s original net book value is $375 ($5,000- ($5,000/40 x 37 years)) with an amortization expense of $125 annually to 2025.

As at April 1, 2022, the asset retirement cost’s net book value is $26 ($300 – ($300/35 x 32 years)) with an amortization expense of $8.5 to 2025. - Using the same information as above, except this building was built in 1975, and estimated useful is 40 years, the building will be fully amortized. As at April 1, 2022, the building would have an original net book value of $0, and the net book value of the asset retirement cost would also be $0.

For unrecognized TCA (for example, Crown lands) the ARO would be expensed, as there is no cost basis of the underlying asset to which the asset retirement can be attached. These include tangible capital assets that do not meet the threshold for capitalization.

For an asset retirement obligation that arises when a tangible capital asset is no longer in productive use (professional judgement should be used to determine whether the asset is to be permanently removed - this includes sale, abandonment, or disposal) or temporarily idling, the cost would be expensed. This is because there will no longer be any period of future benefit attached to the asset.

Measurement

Asset retirement obligations are to be measured as at the date the legal obligation was incurred and must be re-evaluated annually. Professional judgement should be used to determine whether conditions have changed substantially to justify remeasurement.

GREs will have to determine whether a professional assessment should be undertaken based on the benefit versus cost constraint outlined in PS 1000.22.

In the event of re-measurement, the entity is to provide documented substantiation to both the Office of the Auditor General and Office of the Comptroller General.

As per PS 3280.33, the estimate of a liability should include costs directly attributable to asset retirement activities. Costs would include post-retirement operation, maintenance and monitoring that are an integral part of the retirement of the tangible capital asset. The estimate would include costs of tangible capital assets acquired as part of asset retirement activities to the extent those assets have no alternative use.

When assessing whether a present value technique should be applied to the ARO.

Applicable references regarding hazardous building materials:

- Hazardous Waste Regulation (April 1, 1988) – Part 6 – Management of Specific Hazardous Wastes

- Provincial Occupational Health & Safety (OHS) Regulations Part 6 (April 15, 1998)

- Provincial Environmental Management Act, Part 2 (January 1, 1997)

For buildings with asbestos, the measurement date for the legal obligation should be the later of April 1, 1988, or the date the asset was placed in service.

Measurement is based on the best estimate at the financial reporting date of the cost to retire the asset, including removal of hazardous materials. These assumptions can be used to assist in your estimates along with any third-party professional assessments received.

To ensure consistency, entities should reference Citizens’ Services for benchmark rates of application for asbestos, lead, and other hazardous material.

Recoveries

Recoveries should be reviewed in conjunction with the Province’s current policy on recoveries as outlined in H.1.5 Reporting Requirements for Statement of Operations of the CPPM manual.

Recoveries are recognized when all three of the following criteria are met:

- the recovery can be appropriately measured;

- a reasonable estimate of the amount can be made; and

- it is expected that future economic benefits will be obtained.

Recoveries should not be netted against a liability. For fully amortized retirement costs, recoveries are recognized in revenue. For retirement costs not fully amortized, recoveries are recorded in deferred revenue and amortized to external recoveries over the remaining amortization period.

Example:

An Asset Retirement Obligation for dams was established in 2022 for $300. In 2025, the Government of Canada (GoC) established a fund to help offset the retirement costs required by provinces. The GoC has offered to pay half of the costs ($150) to dispose of the dam.

The entry would be:

Dr Cash

Cr Deferred federal contributions

Transitional Provision

In the year of adoption, the Province and associated government reporting entities will adopt a modified retroactive application with full restatement.

In the year of adoption, GREs will recognize:

- A liability for any existing AROs.

- An asset retirement cost capitalized as an increase to the carrying amount of the related tangible capital assets.

- Accumulated amortization on that capitalized cost; and

- An adjustment to the opening balance of the accumulated surplus / deficit resulting from amortization and, IF there is a definitive settlement date, an adjustment for accretion.

GREs with assets no longer in productive use should recognize a liability and a corresponding adjustment to the opening accumulated surplus/deficit.

Those amounts are to be measured using information, assumptions and discount rates as at April 1, 2022. Accumulated amortization, and if applicable accretion, are measured for the period from the date the legal obligation came into effect to March 31, 2022.

Ministry Tracking of Capitalized Assets with AROs

Asset retirement costs are to be tracked within Oracle Fixed Assets (OFA) in accordance with current TCA policy and CAS ARO-OFA guidance provided.

Reporting Requirements

The cumulative ARO balance is presented as other accrued liabilities in the Statement of Financial Position of the Summary Financial Statements.

- Details will be presented as a separate note disclosure of the Summary Financial Statements.

- Entities within the GRE are expected to report all ARO transactions that are recognized in their financial statements as part of their quarterly and year-end reporting requirements on the Supplemental Financial Reporting template or Quarter/Fiscal Year End package to Financial Reporting and Advisory Services (FRAS).

This information is reviewed during the preparation of the consolidated Summary Financial Statements.

OCG Contact Information: Summary@gov.bc.ca

Contact information

Financial Management Branch

OCGMANUALS@gov.bc.ca